|

The information ratio measures the risk-adjusted returns of a financial asset or portfolio relative to a certain index. This ratio aims to show excess returns relative to the benchmark, as well as the consistency in generating the excess returns. The consistency of generating excess returns is measured by the tracking error.

The information ratio is primarily used as a performance measure by fund managers. In addition, it is frequently used to compare the skills and abilities of fund managers with similar investment strategies. The ratio provides investors with insights about the ability of a fund manager to sustain the generation of excess, or even abnormal (as in “abnormally high”), returns over time. Finally, some hedge funds and mutual funds use the information ratio to calculate the fees that they charge their clients (e.g., performance fee).

The information ratio and the Sharpe ratio are similar. Both ratios determine the risk-adjusted returns of a security or portfolio. However, the information ratio measures the risk-adjusted returns relative to a certain benchmark while the Sharpe ratio compares the risk-adjusted returns to the risk-free rate.

Information ratio shows the consistency of the fund manager in generating superior risk adjusted performance. A higher information ratio shows that fund manager has outshined other fund managers and has delivered consistent returns over a specified period.

Description: Information ratio is useful in comparing a group of funds with similar management styles. It is calculated by dividing the active return of a portfolio by the tracking error. The tracking error is calculated as the standard deviation of the difference between fund return and index return.

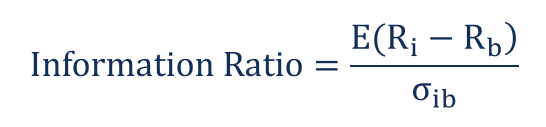

Where:

- Ri – the return of a security or portfolio

- Rb – the return of a benchmark

- E( Ri – Rb) – the expected excess return of a security or portfolio over benchmark

- δib – the standard deviation of a security or portfolio returns from the returns of a benchmark (tracking error)

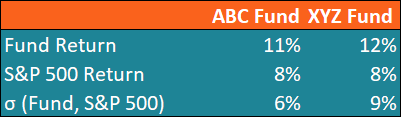

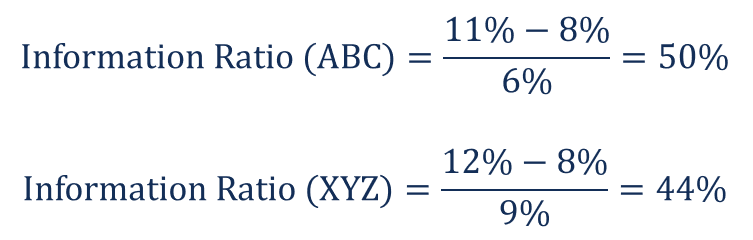

Using the information above, we can calculate the ratios for the funds:

The ABC Fund shows a higher ratio than the XYZ Fund. This indicates that the ABC Fund can more consistently generate excess returns, as compared to the XYZ Fund.

Aucun commentaire:

Enregistrer un commentaire